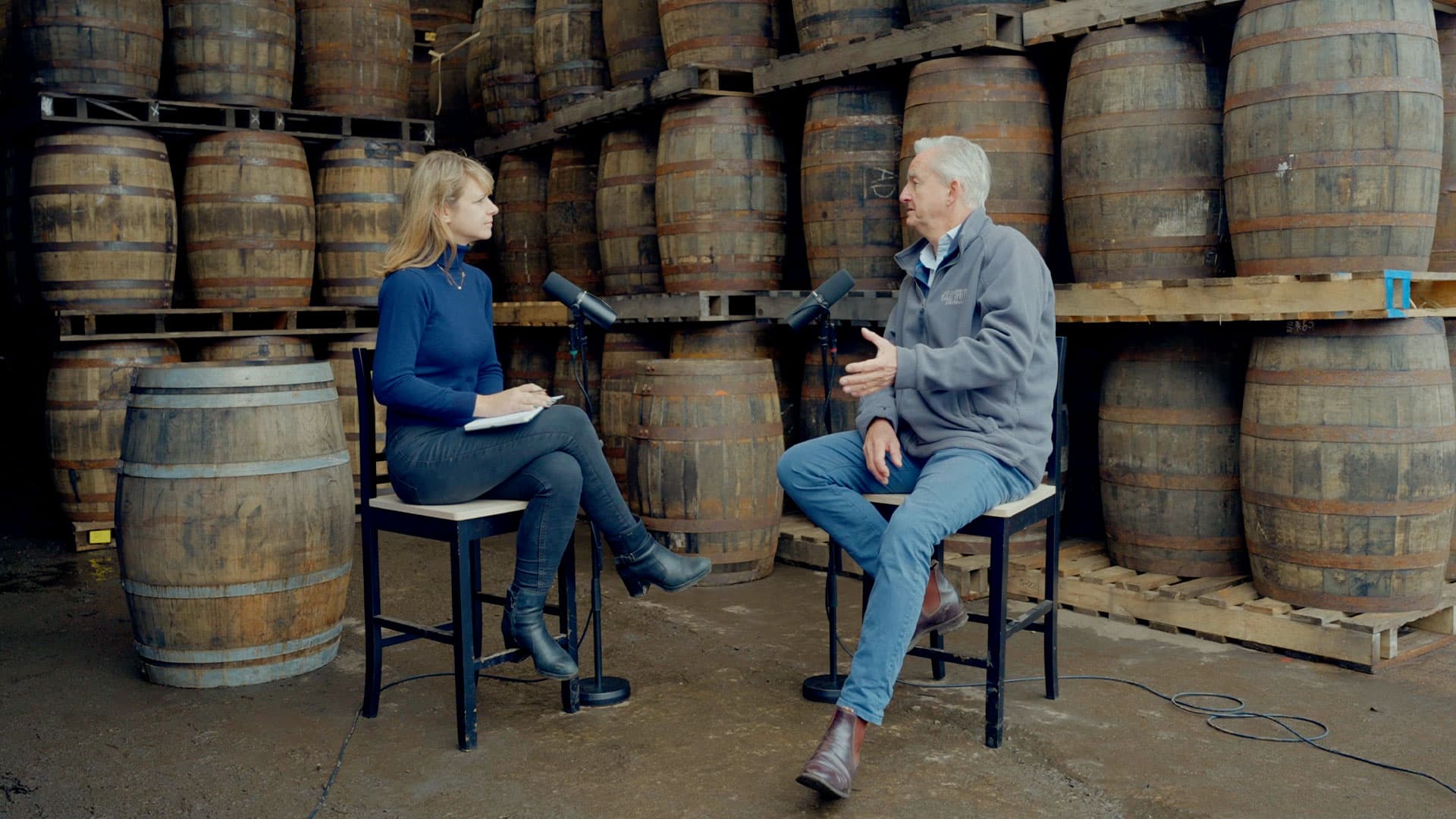

Whisky Investment Podcast S3 E5 – Behind the Scenes: 2025 in Retrospect with Ben Lancaster

2025 In Review, 2026 In Sight: Benjamin Lancaster On Why He Still Backs Whisky

If you only skimmed the headlines in 2025, you would be forgiven for thinking the whisky world was in trouble. Stories about softening luxury demand, oversupply and cautious consumers were everywhere. Yet listening to co-founder Benjamin Lancaster talk to Alwynne Gwilt on the latest episode of The Whisky Investment Podcast, you get a very different picture: a market that is adjusting, and opportunities that still look compelling if you are prepared to think in years rather than news cycles.

As Benjamin tells it, 2025 was not the easiest year to run an alternative investments business, but it was far from a wasted one. The team at VCL Vintners spent much of the year reading past the gloomy soundbites, keeping close to distilleries and bottlers, and quietly putting client capital to work where the numbers still stacked up. “If you’re broadly looking at the industry, it’s definitely had its woes,” he acknowledges, “but from the investment aspect, look, there’s always opportunities… Whisky’s no different… One of the things we, we really made a push on was, was just making sure that we were looking out for opportunities as they come along.”

Beyond the headlines

One of the most striking things in the conversation is how different the view looks from Benjamin’s desk compared with the broader media narrative. Yes, some high-end bottles have cooled and some consumer markets feel cautious, but he is quick to point out that the investment market is not a mirror image of the retail one.

Over the last few years he has seen more liquid flowing into the channels that matter for cask investors. “If you went back five or six years ago, there wasn’t a lot of juice on the market,” he says. “You [look] at the market today, there’s more availability… It is how you look at it. If you look at a headline, but what’s beyond that?”

That extra availability has allowed VCL to tilt slightly towards younger stock, which held its pricing more steadily through recent turbulence, without abandoning the mature casks that still form the backbone of many portfolios. The age on the stencil was less important than the quality of the distillery and the entry price. What mattered was whether a cask, at a given cost, could credibly deliver the outcomes clients were looking for.

Oversupply and the shadow of the eighties

Whenever people talk about more stock in warehouses, the spectre of the 1980s looms. Back then, overproduction, weak demand and a lack of alternative routes to market left the industry with rows of unwanted casks and some very hard decisions.

Benjamin is careful not to dismiss that history, but he makes a strong case that today’s situation is not a simple rerun. The global market for whisky is vastly larger and more diversified than it was four decades ago, and for the first time there is a serious, organised investment layer sitting alongside the traditional bottling trade. As he puts it, “I reckon if you were sitting on casks from the 1980s right now, you’d be pretty happy.” What felt like dead weight at the time has, with the benefit of patience, become some of the most sought-after stock in the system.

That does not mean over-enthusiastic production can never cause problems, but it does underline how perspective changes once time has done its work. What looks like oversupply in one decade can read as scarcity in the next. For Benjamin, the lesson is that context and horizon matter a great deal more than short-term noise.

Looking across the Atlantic

The episode is not confined to Scotland. Benjamin and Alwynne also touch on American whiskey, including the headline-grabbing news that Jim Beam plans to pause production in 2026. At first glance, that sort of announcement can sound alarming. Benjamin’s reaction is more measured. “Yeah, I suppose, but not really,” he says when asked if he was shocked. “It’s a shock when you read the headline naturally, right? Yeah. And you see that and it’s like, okay, but…”

The “but” in this case is important. In his view, this is less a sign of existential distress and more an example of a giant producer managing capacity, warehouse space and future demand curves at a corporate level. “Overall, I don’t think you’d be alarmed,” he adds. “It’s just a case of, well, that’s just where things are at.”

Rather than treat it as a reason to retreat, VCL has been spending more time looking at what is happening in Tennessee and beyond, where some producers appear to be holding steady and where independent bottlers and investors may find room to manoeuvre. It is a useful reminder that even within a single country there is rarely one simple story.

Trade routes, tariffs and the slow burn of policy

Another thread running through the episode is geopolitics. Tariffs and trade agreements are not as eye-catching as bottle auction records, but they quietly shape the landscape that whisky moves through. Benjamin talks about the legacy of bourbon tariffs, the ongoing attempts to hammer out a more favourable trading relationship with India, the loosening of rules in markets such as Hong Kong and fresh recognition for Scotch in parts of Latin America.

None of these developments transform the market overnight. They are more like laying track than running the train. For investors who are thinking about three, five or ten-year horizons, though, they matter a great deal. A tariff cut today may not change a distillery’s bottling run next month, but it can have a very real impact on how easily that liquid finds its way into glasses over the life of a cask. Benjamin’s argument is essentially that this is the timescale on which cask investors should be thinking anyway.

Changing drinking habits, not disappearing demand

It is fashionable to talk about younger drinkers turning away from traditional categories, yet the reality is more nuanced. Benjamin notes that while certain bottle formats or price points are pausing for breath, other areas, particularly ready-to-drink serves, are growing quickly. Major spirits companies are not blind to this and are busy folding core liquids into new formats and new occasions.

From an investment perspective, that distinction matters. A change in how whisky is consumed is not the same as a collapse in whether it is consumed at all. If anything, it underscores the value of strong brands and adaptable producers, which are exactly the type of distilleries VCL tries to work with. The spirit itself still finds its way into the glass; the route it takes is simply evolving.

New distilleries, old names and the question of exit

Looking ahead, Benjamin expects to see more liquid from newer distilleries coming into play, particularly in Scotland, England and Ireland, as they reach the stage of having credible age statements and consistent output. It is an exciting time for drinkers, who will see more choice on shelves, and a potentially interesting one for investors.

At the same time, he is candid about the risks. Anyone can build a still, fill some barrels and sell casks in the early years. The harder part is building a brand that will still be relevant when those casks are ready to be sold on or bottled. “At the same point, where are you going with it?” he asks. “In ten years’ time, if the distillery’s no longer around, it’s a ghost… [and] you’ve still got to find somewhere to try and get it consumed, because ultimately all it just becomes is an asset that matures forever.”

This is why VCL remains anchored to distilleries with proven pedigree and is selective about the newer names it will stand behind. A beautiful spirit in a cask is only half the story; the other half is a credible exit route, backed by a brand that will still mean something when investors are ready to sell.

Returns in a “difficult” year

For all the talk of headwinds, one of the most telling moments in the episode is when Benjamin shares how client portfolios actually performed. He notes that clients made, on average, 13.81 per cent in 2025. It is one of the reasons he says he is confident about the platform VCL has built and the positions they hold.

He is still careful not to overpromise about 2026. “I think the year ahead is one that we are positive about,” he says. “I don’t think it’ll be straightforward, you know, it may not be without its ups and downs, but that’s just the nature of any market, no matter what it is. So I think broadly we’re optimistic.” The combination of increased access to stock, sensible pricing on younger casks, new independent bottling ventures and the slow but steady opening of key markets gives patient investors plenty to be positive about, provided strategy stays disciplined and horizons remain long.

Why this episode is worth a listen

Taken together, the conversation feels like a useful antidote to the more dramatic takes that often dominate discussions around whisky and alternative assets. Rather than calling the top or the bottom of the market, Benjamin is doing something less flashy and more valuable: explaining how an experienced operator is navigating a complex environment in real time, where headlines, trade policy and warehouse inventories all intersect.

If you are already invested in casks, thinking about allocating to the category or simply curious about what is really happening behind the headlines, this episode is well worth your time. It offers a grounded view of 2025, a thoughtful look ahead to 2026 and a reminder that in whisky, as in most things, patience and perspective tend to be rewarded.

Let's talk whisky and spirits.

Connect with our team to explore investment opportunities.

Journal Highlights

Newsletter

Stay ahead of the market. Get access to exclusive offers, events, insights, and news straight to your inbox.